Relative Strength Combine Portfolios upgraded with Composite models

May 20, 2026

in RS Composite

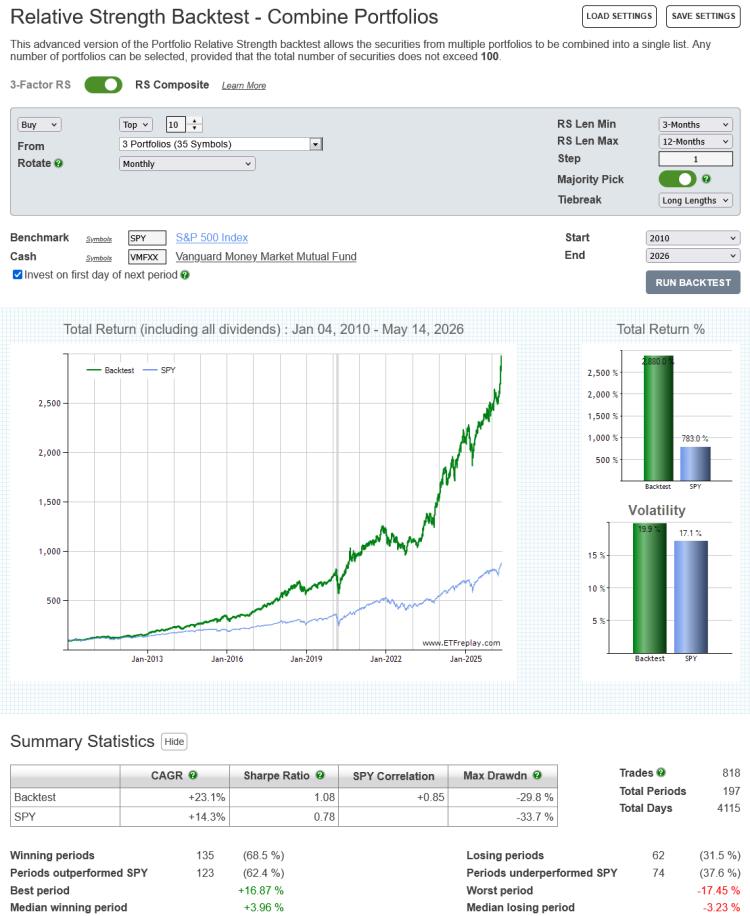

We have enhanced the Relative Strength - Combine Portfolios Backtest by adding the option to test RS Composite models.

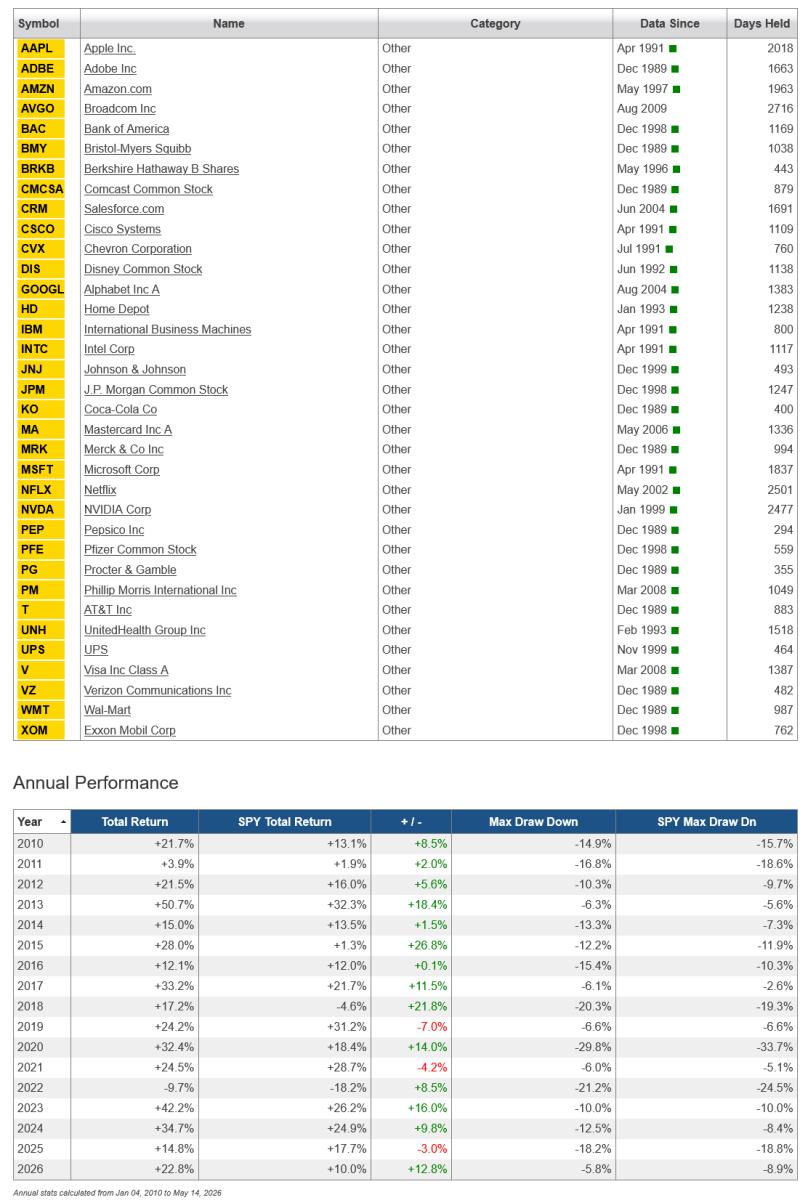

The RS Combine Portfolios Backtest allows multiple portfolios to be combined together into a single list, making it possible to test investing in the strongest (or weakest) security from up to 100 symbols.

Annual subscribers, both pro and regular, now have the option to switch from using 3-factor Relative Strength to an RS Composite model.1

Pro subscribers also have the option to enable the Majority Pick function when running an RS Composite backtest, as per the example below.

click image to view full size version

Go to the Relative Strength - Combine Portfolios Backtest.

Note:

1. For more details on the difference between the 3-factor Relative Strength model and RS Composite, see Relative Strength: 3 Factor vs Composite

Follow ETFreplay on