New Relative Strength Composite Backtest

Jan 30, 2023

in RS Composite

We have added a new backtest, Relative Strength Composite, which can protect against parameter choice misfortune by making it easy to diversify across a range of lookback values.

When relying solely on a single lookback period, though it may have backtested well, there's always the possibility that it may underperform in the future. The RS Composite backtest attenuates that risk by stepping through the return lookback periods, from your chosen minimum to maximum, and invests in the top (or bottom) x securities from each.

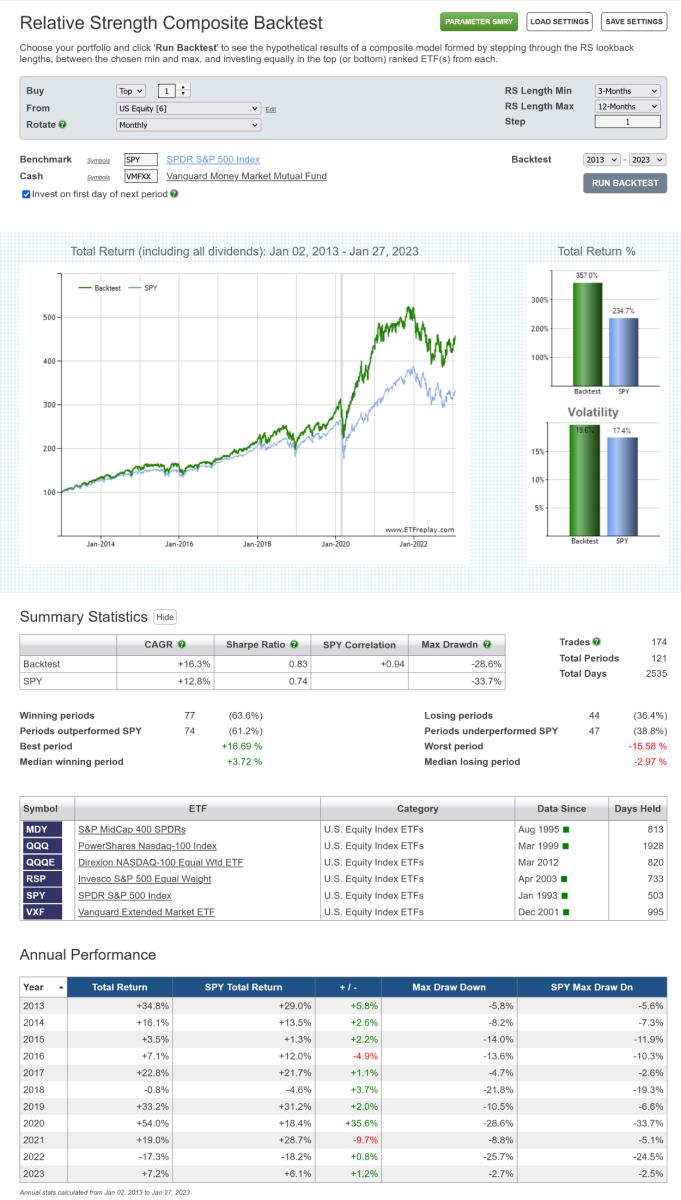

In the following example, the minimum length is 3-months, the maximum lookback is 12-months and the step value is 1. This means that, each month, the backtest will invest 10% in each of:

- Top security ranked by 3-month returns

- Top security ranked by 4-month returns

- …5-month returns

- …6-month returns

- …7-month returns

- …8-month returns

- …9-month returns

- …10-month returns

- …11-month returns

- Top security ranked by 12-month returns

click image to view full size version

The step value can be increased to assess whether it is possible to retain a significant degree of diversification without needing to employ every return length. For instance, raising the step value to 3 in the above example will mean that the backtest ranks the portfolio ETFs by 3, 6, 9 and 12-month returns each month and invests 25% in the top ranked security from each of those.

Watch video: How to use Composite Relative Strength

The Relative Strength Composite backtest is available to annual subscribers, both regular and pro.

Note:

- Just as a diversified portfolio means that some part of it will always be a drag, a composite of model variants will always underperform the single best version of a strategy....but it also avoids being exclusively in the worst.

- To see how each of the return lengths performed individually, rather than as a composite, use the RS Parameter Performance Summary

Follow ETFreplay on