Dec 05, 2017

in Relative Strength, Video

A short video using the Advanced RS Pro backtest to look at how mixing strategies together performed during the 2000-2002 and 2008 bear markets..

to expand, click the '4 expanding arrows' icon in the bottom right corner of the video screen

Dec 04, 2017

We have just introduced a new subscription package for investing professionals.

Based on feedback and requests the we've received from advisors and portfolio managers, the new pro subscription adds the following functionality to the regular subscription.:

- All Moving Average, Channel, Ratio and Relative Strength portfolio strategies can be backtested from Dec 31, 1999

- Buy Top limit on all Relative Strength backtests raised to 20

- Number of favorite backtest settings to Save / Load increased to 20 per backtest

- Number of Dashboards increased to 20

- Advanced Relative Strength Pro backtest: test investing the strongest ETFs from up to 4 separate portfolios

- Core-Regime Relative Strength & Core-Regime Portfolios backtests

- Annual fee deduction option on Core-Satellite, Core-Regime RS and Adv RS Pro backtests

- MA Filter on Core-Satellite & Adv RS Pro can be Daily or Monthly MA

Subscribers that would like to upgrade to this new package can do so by going to My Account > Subscription Settings > Upgrade to Pro

Nov 02, 2017

in Backtest

If you would like to test Short-Selling on ETFreplay, use the versatile app called Rel Str - Combine Portfolios.

You can test going short the top or bottom ranking securities in a list.

Oct 06, 2017

in Regime Change

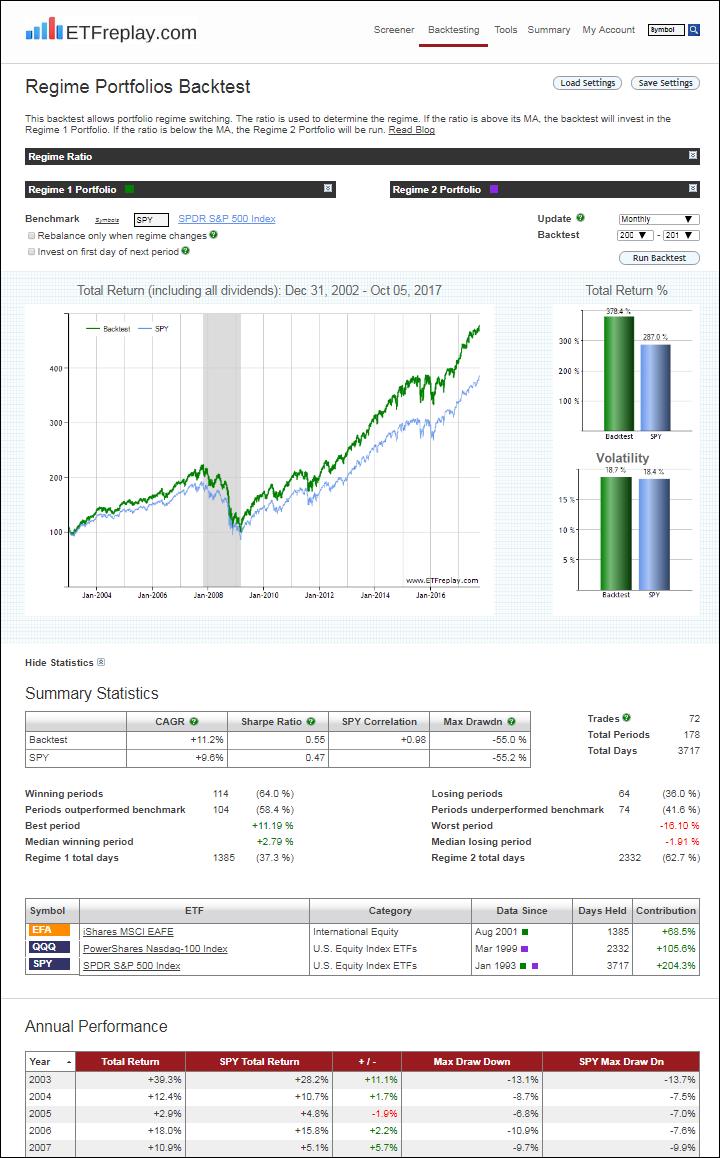

This backtest defines a Regime by comparing the performance of EFA and QQQ, two standard ETFs with plenty of market cap. The backtest then decides to allocate to EFA or QQQ depending on which Regime is in place. SPY is held in either case as a core position:

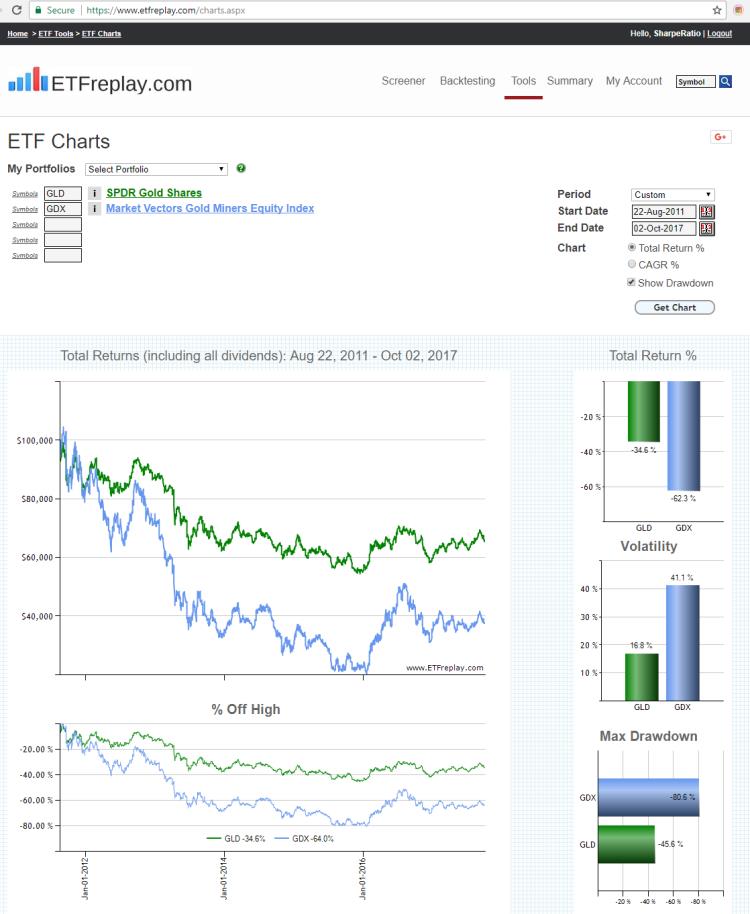

Oct 03, 2017

in Drawdown