Category: Parameter Summary

Apr 08, 2025

in Channel, Parameter Summary

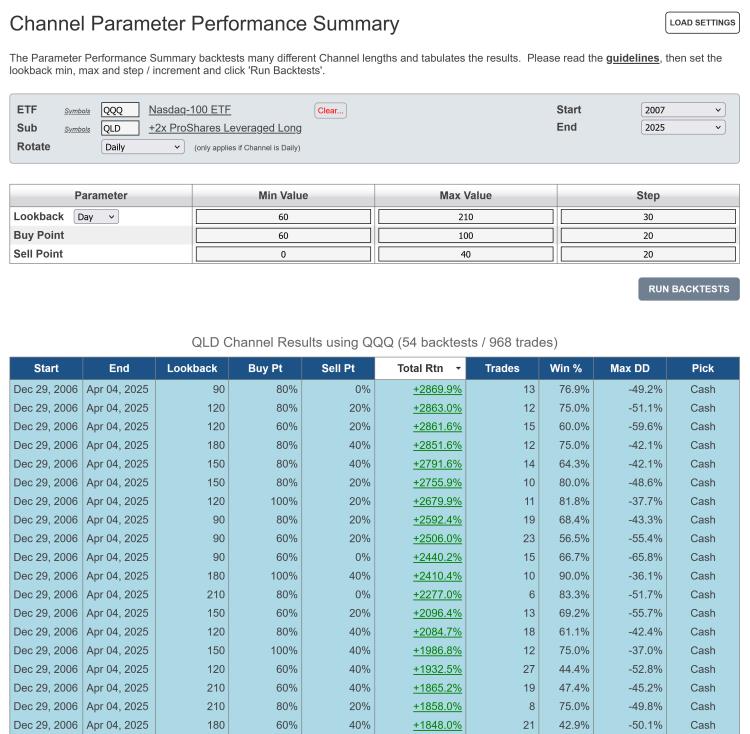

We have made two upgrades to the Channel Parameter Performance Summary.

Firstly, the Channel Parameter Summary now allows a range of Buy and Sell points to be tested. Whereas previously only a single Buy and Sell point could be specified, it is now possible to set min, max and step values for these two parameters.

Secondly, a Substitute function has been added, which allows a different / replacement security to be specified for the execution of the actual trades. For example, a channel can be based on the Total Return value of QQQ, but the resulting trades can be executed in QLD.

click images to view full size versions

Go to the Channel Parameter Performance Summary

Notes:

- Studying the guidelines is strongly recommended.

- Parameter Performance Summaries are available to both regular and pro annual subscribers

Jul 28, 2023

in Drawdown, Parameter Summary

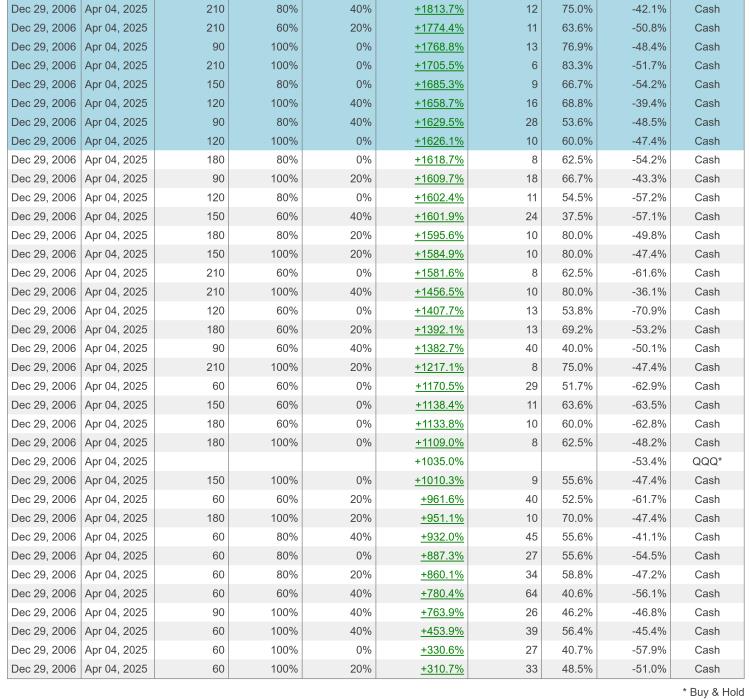

We have expanded the range of backtest statistics produced by the Parameter Performance Summaries with the addition of max drawdown.

The Parameter Performance Summaries make it possible to backtest numerous different parameter values in one go and assess the results. The table of backtest results is ordered by total return by default, but can now also be sorted by max drawdown (Max DD) as well as by win percentage, parameter value etc.

The Parameter Performance Summaries are available to both regular and pro annual subscribers:

As always, studying the guidelines that we published within the original Parameter Summaries announcement is highly recommended.

Feb 08, 2023

in Video, Parameter Summary, RS Composite

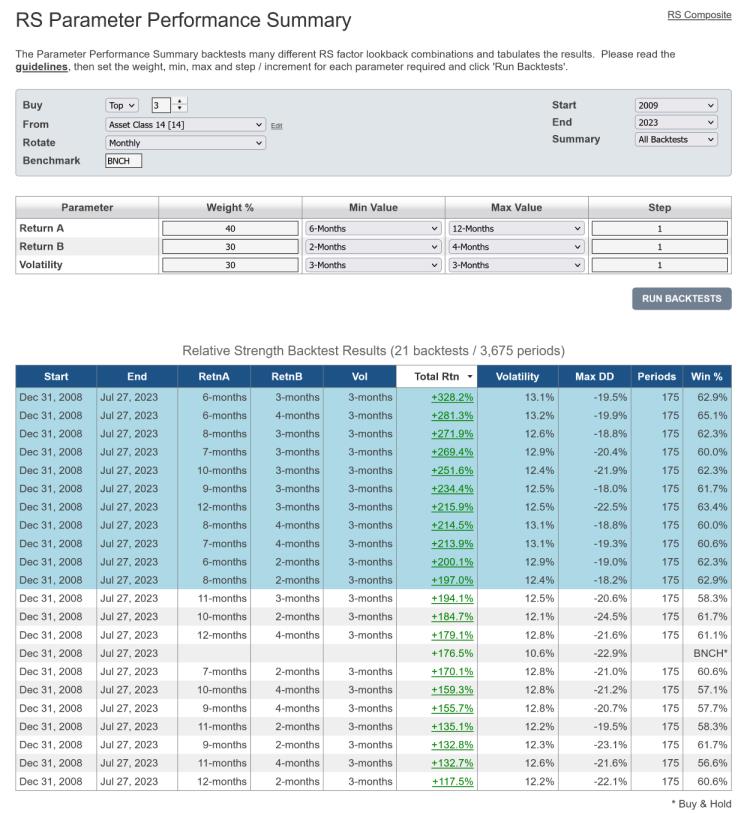

Instructional video on how to use Composite Relative Strength to improve your ETF backtesting process. #STUDY

to expand video on screen, click the '4 expanding arrows' icon in the bottom right corner of the video screen. Use the settings icon to change to 1080 quality if it seems at all blurry

See also: RS Parameter Performance Summary

Oct 17, 2021

in Backtest, Relative Strength, TRD Total Return Diff, Video, Ratio, Parameter Summary

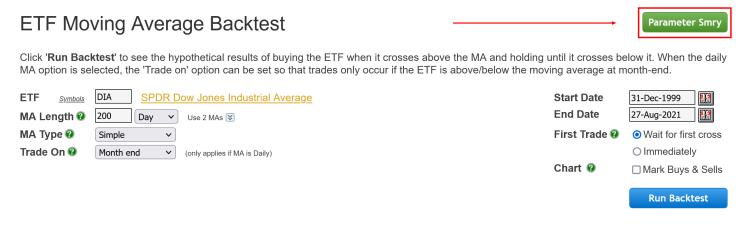

Instructional video on how to use the Parameter Performance Summary functionality. #STUDY

to expand video on screen, click the '4 expanding arrows' icon in the bottom right corner of the video screen. Use the settings icon to change to 1080 quality if it seems at all blurry

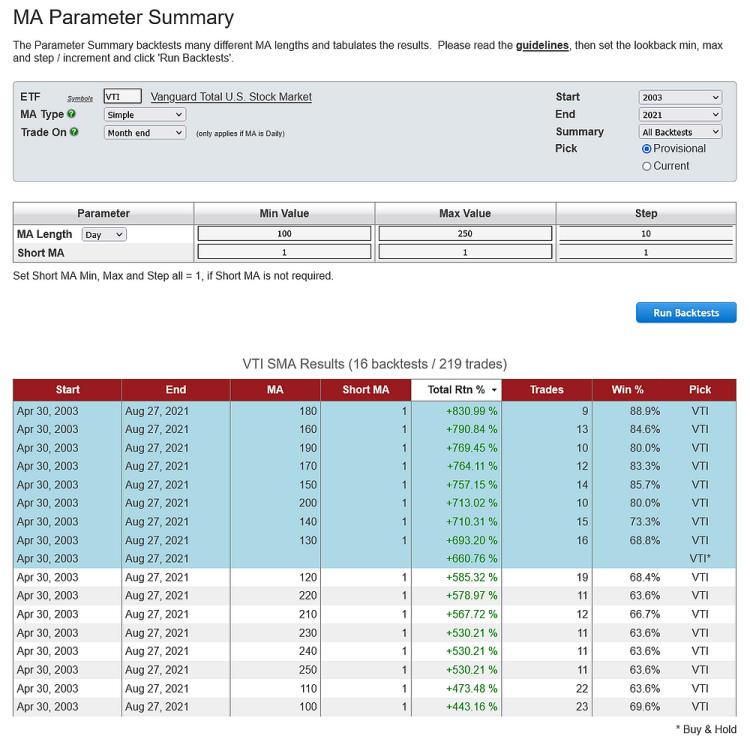

Aug 31, 2021

in Backtest, Moving Average, Channel, Ratio, Parameter Summary

We have added three new Parameter Performance Summaries to the website:

As with the Relative Strength and TRD summaries that we introduced in July, each of the above can be accessed from their respective backtests.

Set the min, max and step / increment for each parameter, then click 'Run Backtests' and the tabulated results will be displayed:

Parameter Performance Summaries are available to all (regular and pro) annual subscribers.

** studying the guidelines that we published within the original Parameter Summaries announcement is highly recommended **