Indexes Change Over Time. Recent Data Is More Important Than Long-Term Data. It just is.

Jan 18, 2018

in Regime Change

An index can change rather importantly over time. Some segments go through sustained secular performance and become increasingly important on a secular basis. This has happened with the internet relative to much older industries. Sometimes it can be a bubble but for every time someone calls something irrational, there are many cases where something secular is happening.

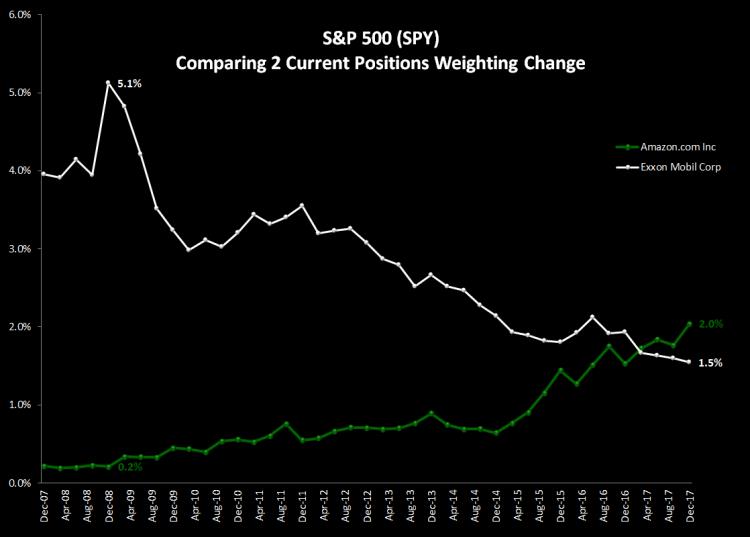

Below is a chart plotting how much more important Amazon.com is to the performance of the S&P 500 than it used to be. This has come at the expense of names like Exxon.

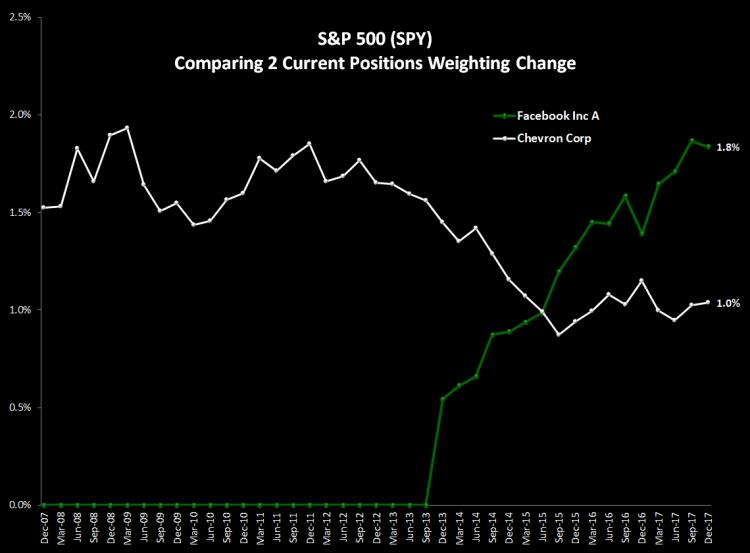

Another example is Facebook vs Chevron:

To look at a different part of the world, think about how important China Mobile used to be vs where it is now and how Alibaba Group was 0% and now its the 2nd largest holding in the S&P China Index.

Think about what this does to fundamental ratios like P/E's and dividend yields on the index aggregates. Exxon pays a large dividend -- AMZN and FB don't pay anything in dividends. Exxons P/E in 2007 was under 13x while the AMZN P/E has averaged well into the triple digits over the past 10 years.

This is loosely related to 'Regime Change' -- the fundamentals of backtesting are that you should think about RECENT DATA and weight it more heavily than old data. Same concept. What the P/E was 10 years ago isn't very important And what it was 30 years ago is less important than that. We do NOT mean to imply 'this time is different'. We are simply saying weight more recent times more highly than you do data from 100 years ago.

See also: Regime Change Backtesting

Follow ETFreplay on