Category: Regime Change

Mar 20, 2018

in Regime Change, Video

A video using the Regime Portfolios Backtest to check-in on using high-yield bonds as information into the state of the market.

to expand video on screen, click the '4 expanding arrows' icon in the bottom right corner of the video screen

Jan 18, 2018

in Regime Change

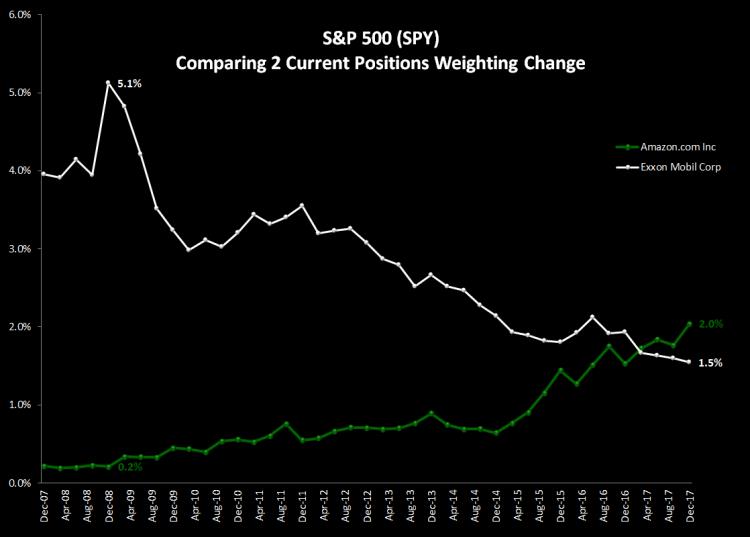

An index can change rather importantly over time. Some segments go through sustained secular performance and become increasingly important on a secular basis. This has happened with the internet relative to much older industries. Sometimes it can be a bubble but for every time someone calls something irrational, there are many cases where something secular is happening.

Below is a chart plotting how much more important Amazon.com is to the performance of the S&P 500 than it used to be. This has come at the expense of names like Exxon.

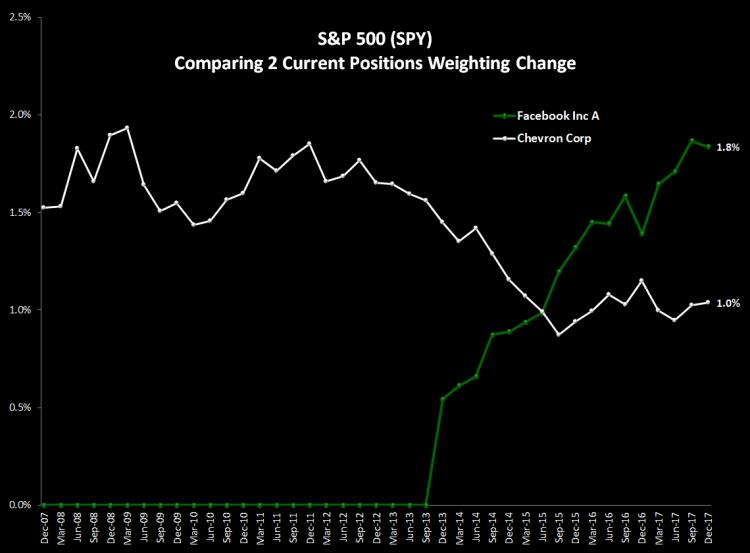

Another example is Facebook vs Chevron:

To look at a different part of the world, think about how important China Mobile used to be vs where it is now and how Alibaba Group was 0% and now its the 2nd largest holding in the S&P China Index.

Think about what this does to fundamental ratios like P/E's and dividend yields on the index aggregates. Exxon pays a large dividend -- AMZN and FB don't pay anything in dividends. Exxons P/E in 2007 was under 13x while the AMZN P/E has averaged well into the triple digits over the past 10 years.

This is loosely related to 'Regime Change' -- the fundamentals of backtesting are that you should think about RECENT DATA and weight it more heavily than old data. Same concept. What the P/E was 10 years ago isn't very important And what it was 30 years ago is less important than that. We do NOT mean to imply 'this time is different'. We are simply saying weight more recent times more highly than you do data from 100 years ago.

See also: Regime Change Backtesting

Oct 06, 2017

in Regime Change

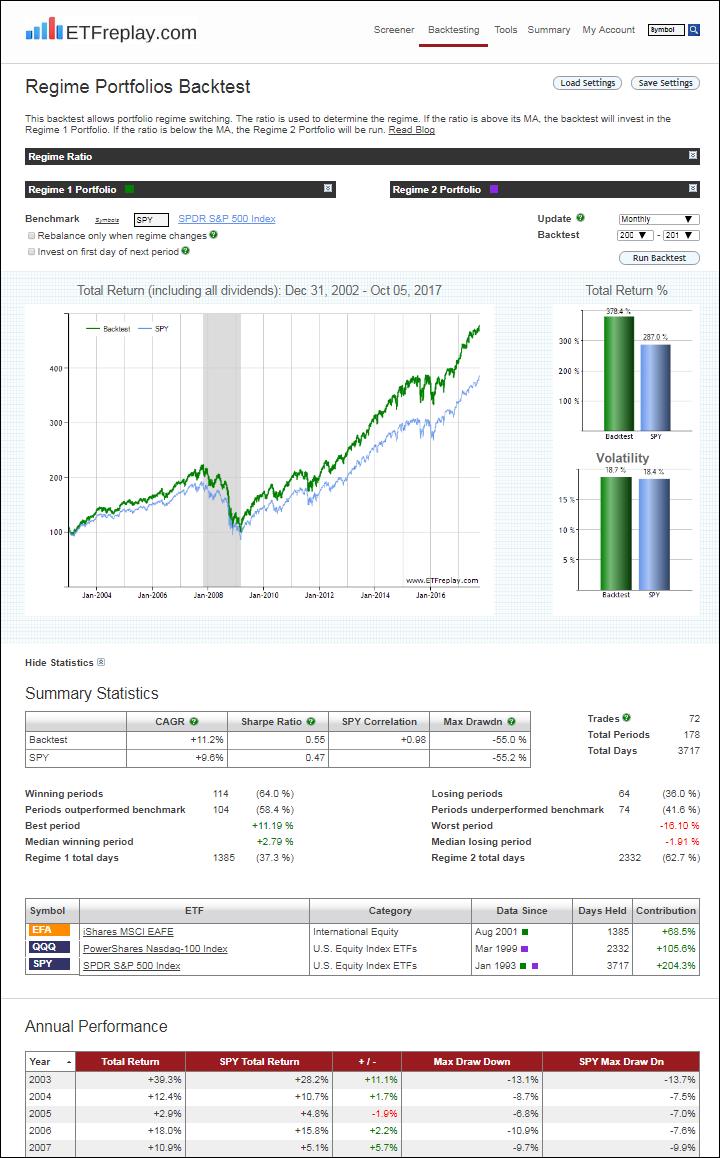

This backtest defines a Regime by comparing the performance of EFA and QQQ, two standard ETFs with plenty of market cap. The backtest then decides to allocate to EFA or QQQ depending on which Regime is in place. SPY is held in either case as a core position:

Jan 23, 2017

in Regime Change, Ratio

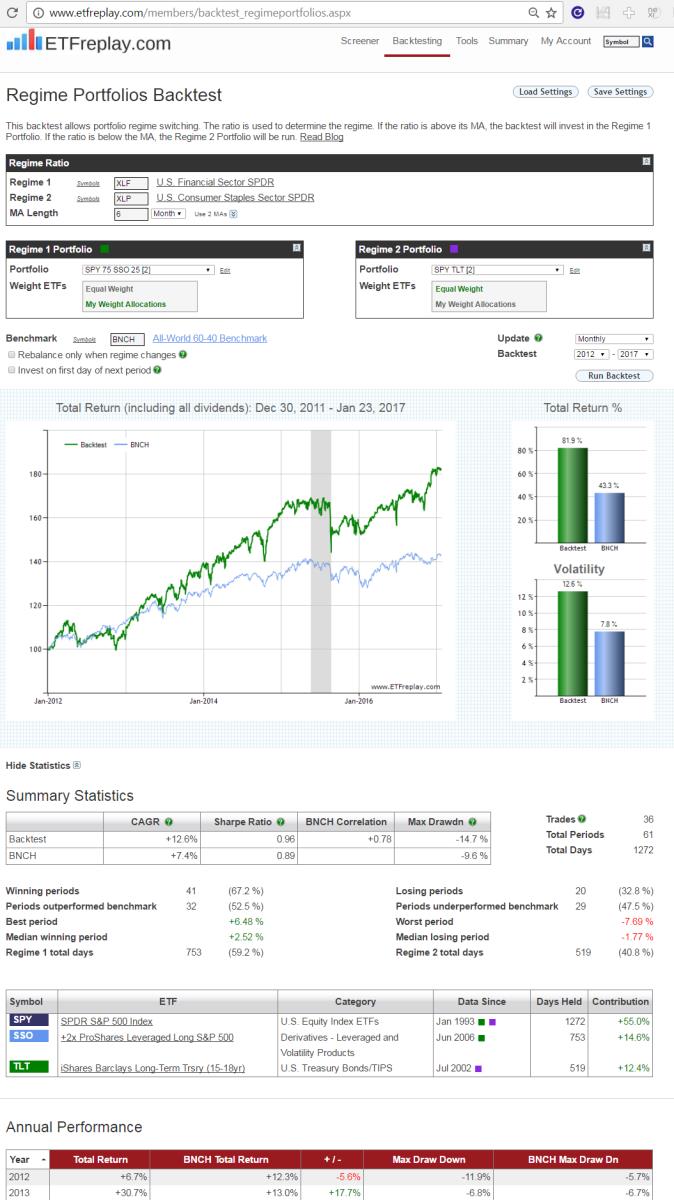

Last month we did a blog post on using high-yield bonds as a key indicator. This month we continue with a focus of using financial stock ETFs as a second indicator.

Many people seem to want to try to simplify everything down to one variable -- often something like a P/E ratio or a moving average. We think investors should look at a range of important indicators and then take a weight-of-the-evidence approach. Indeed, we built ETFreplay.com so that you can easily run and update a list of strategies AND do this on a continuous basis and thereby stay in tune with the overall structure of the market.

There is no better information than that which the market itself generates. A good market participant will learn to read what the market structure is telling you by analyzing its intermarket relationsihps.

Financial companies have business models that make our economy go. From mortgages and credit cards for individuals to bank loans and payment services for corporations, financial companies are absolutely vital indicators on overall conditions and this is why these companies are regulated closely by government agencies.

It makes sense that when financial stocks are doing well, how bad can the market environment be?? Look back at past recessions and you will see very poor performance of financial stocks.

The backtest below is meant as an INDICATOR -- not a strategy to implement per se.

When financial stocks are beating a known risk-off stable segment like US Consumer Staples, we will bring our portfolio Beta up above 1.00 by adding a 25% position in SSO (the 2x S&P 500 ETF).

When financial stocks are underperforming, we will split our holdings into 50% SPY and 50% TLT. This is the 'risk-off' portfolio. (Note that in this example -- no matter which regime is in play, the portfolio will hold at LEAST 50% SPY -- think of that as the 'core' portfolio and the other 50% as the 'satellite').

Here are the results. Make sure to dive-in and immerse yourself in this topic. Alter the time periods incrementally. Alter the risk-on risk-off portfolios. Study sub-period backtests. What are the good aspects to this backtest? What are the possible limitations?

Dec 02, 2016

in Regime Change

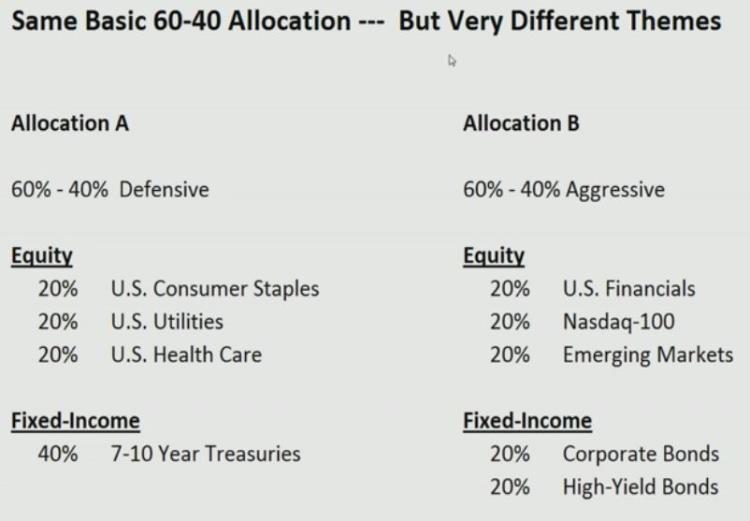

Back in 2011 we produced a little video that compared the performance of two very different 60-40 allocations: an aggressive portfolio invested in Emerging Markets, Financials and High Yield; and a defensive strategy based around Treasury Bonds, Utilities and Healthcare.

The purpose of that video, was not to show which allocation was best but rather to illustrate that 'that different sectors perform differently during the course of the business cycle'. It therefore makes sense that when there is a change in the overall regime, allocations should be materially adjusted.

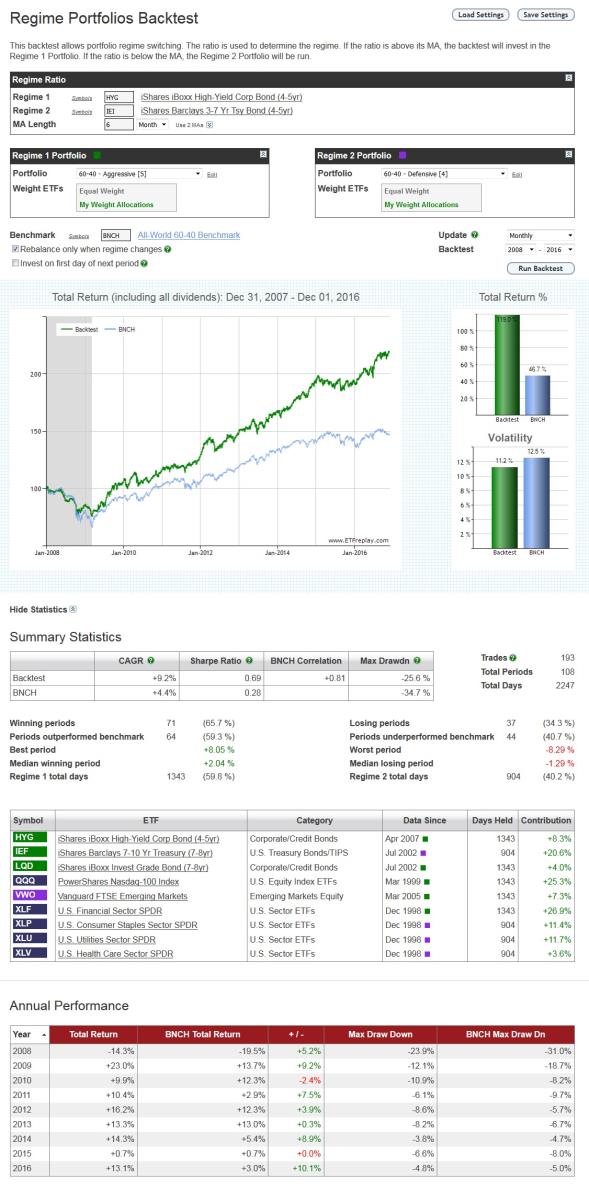

Below is an update to that original example. The same two aggressive and defensive allocations are used, but this time we have employed the Regime Portfolios Backtest to dynamically switch between them depending on the prevailing regime. For this example with have used a simple credit spread style ratio to define the regime. When high yield bonds are outperforming treasuries, the backtest invests in the aggressive allocation. When the opposite is true, it switches to the defensive portfolio.

This is not meant to be a comprehensive strategy by any means, it's just a simple example to illustrate the concept of adapting to change. Hopefully though it provides a solid starting point for subscribers to conduct their own regime based research.