Nov 24, 2010

In old-school financial theory, ‘the market’ was often assumed to be the S&P 500. Many people in the financial industry grew up on defining things (like Beta –> and therefore Alpha) relative to the S&P 500. This wasn’t the correct interpretation from Modern Portfolio Theory --- but as the 1990’s bull market raged, the question was not about U.S. equities vs bonds vs international investing or anything else --- it was more a discussion of simply ‘which US equities?’ – and the popularization of ‘style boxes’ that carved up the U.S. market according to size (small , mid or large cap) and style (value vs core vs growth).

In 1998, the S&P 500 rallied 25%+ while small cap U.S. stocks were essentially flat. The dispersions between picking segments of the U.S. were very important then. Much discussion was also whether you were overweight technology – or underweight sector XYZ – all along assuming that of course your universe was U.S. equities. The economy was robust and it was not unusual for companies to grow 5-10%+ every 90 days (sequential quarterly growth).

Those days of course are long gone. The companies growing 5-10%+ every 90 days now are more likely located in Brazil or India etc… Still, the dispersions between market segments can be very large. The conversation doesn’t end at --- overweight bonds --- but which bonds? Long-duration corporates or intermediate high-yield -- or preferred stocks for that matter? Overweight international stocks? Which international stocks – what regions, which countries?

One very interesting aspect of ETFs is that they allow allocations to be adjusted not just easily – but with such precision and at essentially no cost. Expense ratios are in the 0.40% zone and are already accounted for in market prices. With free trading now available --- it just gets better.

But ETF investing doesn’t have to end at allocation decisions. ETF rotation involves rotating beta exposures over time. Its not just about picking a low-cost allocation and sticking to it. Surely you have some view on some market segment in some region of the world?

Importantly, expressing this view can be done as a satellite rotation strategy against a core portfolio of conservative investments, or on its own. Its up to you and your risk tolerance and any other constraints you impose.

The point is that there is tremendous value to be added that has nothing to do with stock-picking. ETF's allow us to operate at a level that is above stock-picking – and picking market segments has and always will be more important than stock-picking.

Even with all the ‘insider networks’ of professional money managers --- hedge fund indexes have shown very mediocre net performance, with any benefits of outperforming funds accruing primarily to the hedge fund manager -- and not to the investor. Moreover, the data to fully risk-adjust these performances just isn’t available without a daily NAV – something hedge funds do not report.

So here we have transparent, ultra low expense ratio, free trading vehicles that operate at a level far more important than adding (or subtracting) 2.00% in stock-picking.

To quote a recent line I heard from a high-profile CEO: “Get on the bus.”

Nov 21, 2010

in Relative Strength, Screener

We have received this question a number of times in email and so we wanted to clarify something.

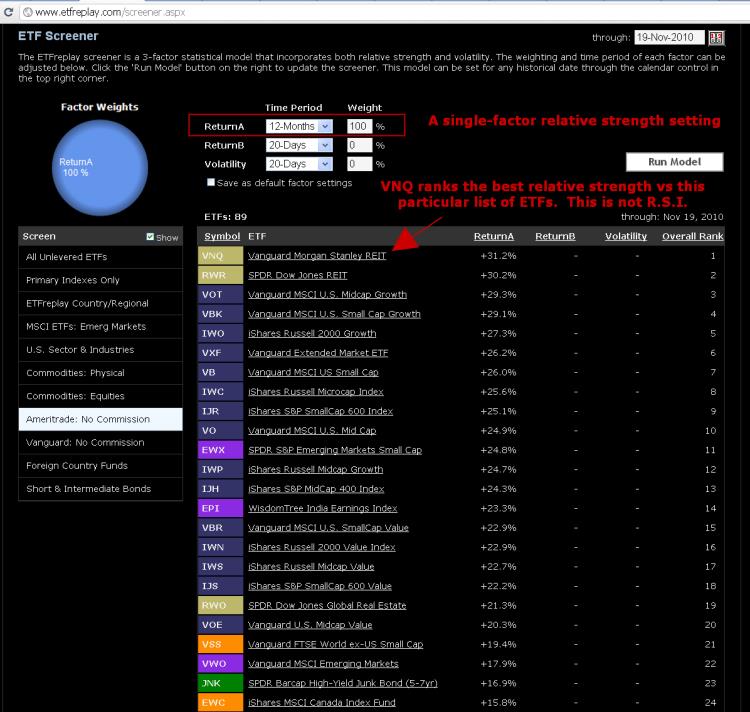

R.S.I. (known as the Relative Strength Index) and the way we at ETFreplay.com discuss ‘Relative Strength’ are not the same thing. We wanted to briefly explain this.

R.S.I. is a technical analysis tool that involves only a single security -- it measures the average amount of up closes vs the average down closes over a given period of time. The most important distinction here is that R.S.I. only looks at the closing values of one security. There is nothing in the calculation of R.S.I. that involves anything but the historical prices of this SINGLE security.

The way ETFreplay uses relative strength has nothing to do with R.S.I. We use relative strength as a way to determine which among multiple market segments is relatively strong.

Many of you are probably familiar with Investors Business Daily. The paper has for a long period of time used a ‘RS Rank’ --- this is more like what we use. Note that IBD certainly did not invent the concept of relative strength -- but they built a database of securities and then ranked everything relative to each other. Institutional-oriented software programs do the same thing. A RS Rank of 90 in IBDs method means that a stock has outperformed 90% of the other securities in their database over a given period of time. High-end institutional software does something similar – except they proceed more mathematically by instead expressing the strength of the security as the distance from the average of a group --- and this is usually stated in terms of the # of standard deviations away from the mean (think z-score).

This is all similar to what we have done – except we do it with ETFs and then allow you to backtest it yourself rather than just saying ‘you should buy relative strength because it works.’ We also allow the user to define relative strength themselves – using easy browser controls like drop-down menus and text boxes. So for example you could simulate IBD’s method by using 12-month performance and ranking ETFs in a given universe like this:

click image to view full size version

Then you could go the Portfolio Relative Strength backtest to see how 12-month relative strength has been holding up over the past 10+ years and see what kind of drawdowns its had.

This is all a research process – its just that we are performing research that comes in a very practical form. We aren’t researching stocks, we are researching strategies --- strategies based on baskets of stocks. Backtesting is not the only thing that matters --- but its pretty darn good information for you to factor into your decision-making process. Without some historical testing, you could easily go a lifetime of doing things that you thought worked – but actually don’t -- and never really did.

Go to the Screener

See also: Relative Strength: 3 Factor vs Composite

Not a subscriber? Subscribe

Oct 20, 2010

in Relative Strength

We showed a few examples of some very basic relative strength techniques at a recent investor event.

This example was meant to show a relative strength strategy that easily could have been thought of as unbiased at any point in past 10 years -- or right now for that matter.

For simplicity, we have used the global regional ETFs and have simply covered the major parts of the 'developed world'. We know that emerging markets have been excellent performers over the past 7-8 years -- as have selected other assets like Gold -- but we have intentionally left these out. We wanted to show something that had some poor performing picks, a few good ones and therefore representative of someone who didn't pick ETFs particularly well but implemented a sound technique to stay with leaders and avoid large underperformers.

Importantly, we believe investors SHOULD decide first which ETFs they would like to be involved with and exclude those they have no interest in on a fundamental basis -- this is value-add to a basic, mechanical technique such as this.

So for this example we use the World Index as a starting point and seek to just 'cover' the developed regions:

Current Approximate Weightings in Global Indexes are:

| United States |

42.0% |

| Developed Europe |

25.0% |

| Japan |

7.0% |

| Developed Pacific [1] |

7.0% |

| Canada |

4.5% |

***Emerging Markets Excluded

[1] Developed Pacific is ~97% Australia/Hong Kong/Singapore and 3% 'other' (New Zealand etc..)

From an indexing perspective, Canada is always kind of the lonely child. Canada is generally not included within a broader regional ETF -- and is not generally lumped with the United States for a North American ETF. For conservatism here, I will exclude Canada and use the first 4 only. These are logical regions in our view. We get coverage of many different countries within this regional framework so this seems quite fair and hardly something that could not have been thought of many years ago -- or even today.

We will include the first 4 from above and SHY, a <2-year duration U.S. Treasury ETF which will act as a benchmark for positive returns. If no region of the world is beating 2-year maturity short-term fixed-income -- then SHY will by default be thought to be the highest Relative Strength ETF.

Here is the result using a 6-mo / 3-mo 2-factor relative strength model with monthly re-balancing.

Note all historical results are purely hypothetical and meant to show the mechanics of the backtesting application. This does not represent investment advice.

Symbol list here is: SPY, EWJ, IEV, EPP, SHY

Sep 20, 2010

in Moving Average

If you have created a portfolio list on ETFreplay, we are building new applications to leverage your ETF lists.

We have two new modules out that we have been working on for the past few months. These applications offer simplified views to help us try to understand larger forces at work in the global marketplace.

Building upon academic research regarding the use of moving averages, these apps save investors time by allowing many calculations and quantitative analyses to be simplified into a few clicks. We think that creating specific entry/exit rules and creating a detailed strategy report adds value to better understanding a concept. That is, we create apps that convert concepts into tangible, specific techniques. The accountability of these techniques is built into the very architecture of the website. On any day, you are just a click away from an updated view of the profit and loss history of a particular strategy.

Importantly, this type of research should be used as a complement to other forms of research. We suggest you think about which types of ETFs you want to be involved with over the long-run and then use techniques such as relative strength and moving average backtesting to help you research methods that reduce risk of a large drawdown, while potentially offering to enhance your return as well.

ETFreplay.com/backtest.aspx

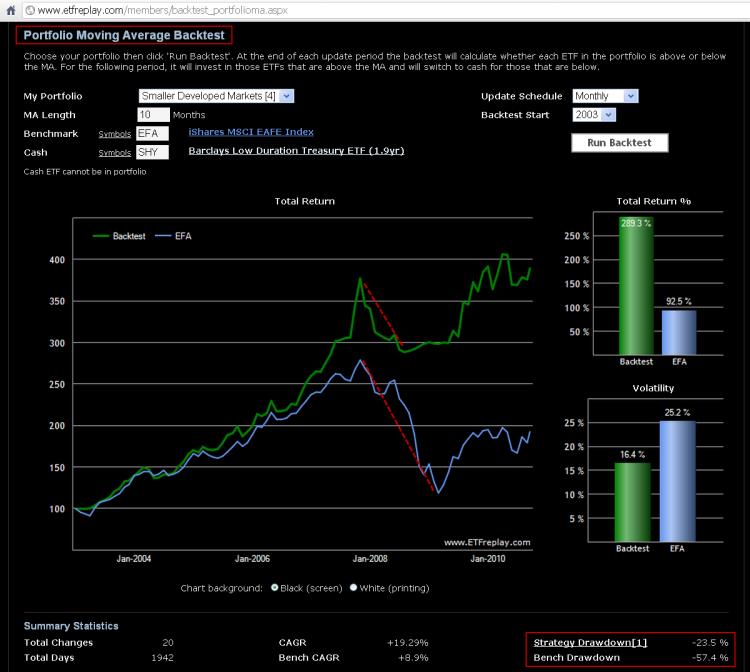

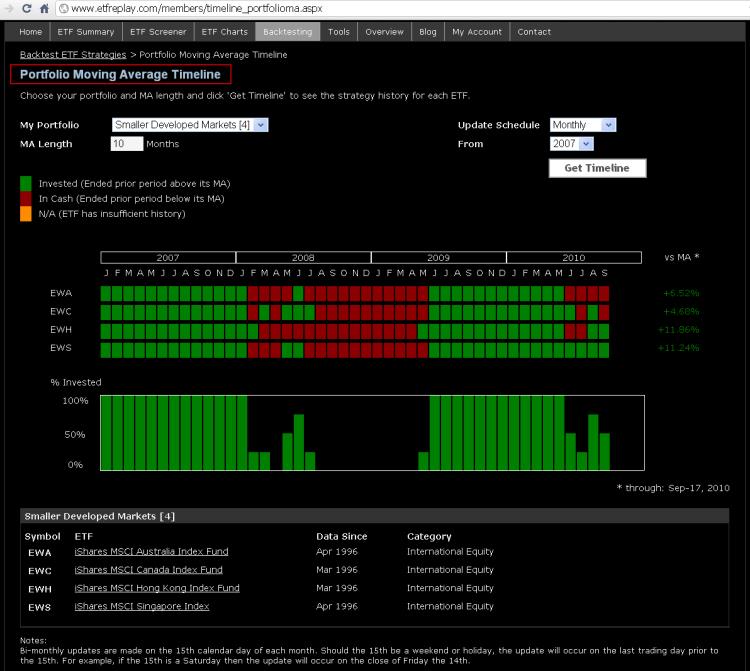

The example below uses 4 key smaller developed markets outside Europe & the U.S.

1. EWA iShares MSCI Australia Index

2. EWC iShares MSCI Canada Index

3. EWH iShares MSCI Hong Kong Index

4. EWS iShares MSCI Singapore Index

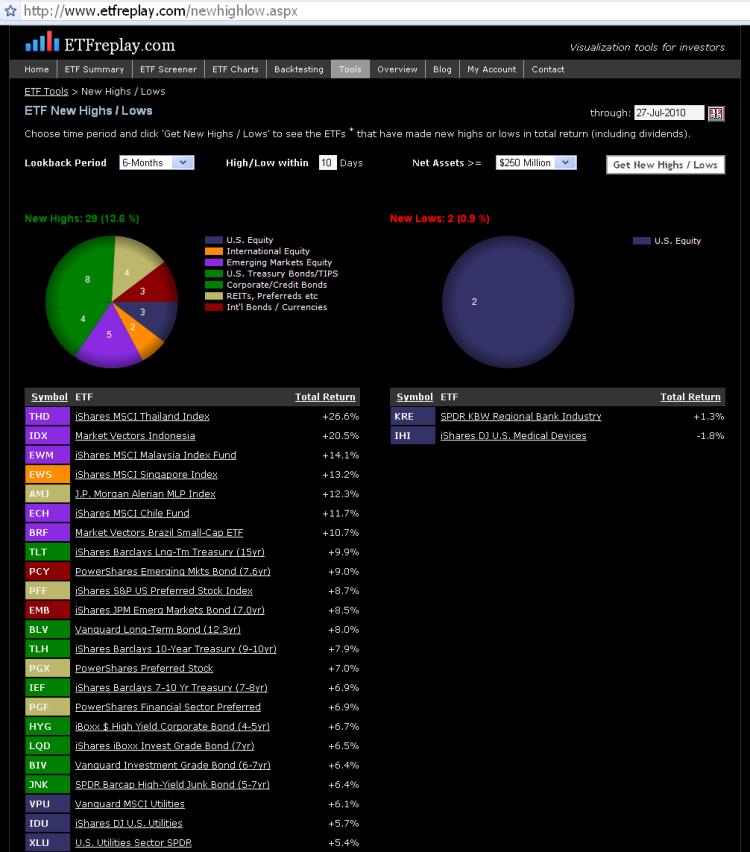

Jul 28, 2010

in Relative Strength

This summer is a good reminder that ETF investing does not revolve exclusively around equities. After assuming a leadership role in early May, many non-equity forms of ETFs have made repeated new highs over the past few months. Treasury Bond ETFs have been the most obvious example of relative strength but other groups performing well include: the Master Limited Partnership products (AMJ), Emerging Market Bond ETFs (EMB, PCY), Preferred Stock ETFs (PFF,PGX, PGF) and more recently, U.S. Utility Stock ETFs (XLU, IDU, VPU).

What do the majority of these ETFs have in common? Most of the recent 6-month ETF list of new highs involves indexes associated with yield (and lower relative volatility vs the S&P 500).

Try the interactive functionality of the above webpage here: New Highs and Lows App

With regard to equities, we’ve seen some new multi-month highs made in some select Asian and Latin American equity indexes. We will be watching to see to what extent other equity country funds can confirm this new potential leadership area (emerging markets equity).

U.S. stocks made fresh six-month lows at the beginning of this month. The drawdowns of some of the primary indexes this year have been -15.7% for the S&P 500, -20.1% for the Russell 2000 (IWM) and -22.8% for the Vanguard Europe ETF (VGK) (drawdown is the maximum high to low correction using closing prices). These groups have rallied hard over the past 20 days but they appear to be in a holding pattern as evidenced by their poor/mediocre rankings on 3 & 6 month relative strength lists.

Another important item to point out is that owning bonds and yield-oriented hybrid securities (like those listed above) has been a LOWER volatility method to making money these past few months.

When the market gets volatile – as it does during corrections – buying inverse ETFs may seem like a good way to make money -- but remember, the Sharpe Ratio penalizes for volatility and you must expect large returns to offset taking on such rising volatility environments. Short-sellers have been punished hard this month while lower volatility funds (like those listed above) have appreciated.

In some respects, owning bonds -- particularly treasuries -- is a dominant method over shorting stocks. The volatilities are far lower if you keep your maturities reasonable. Thus you can express a bearish view without taking the same risk as you do during hard short-squeezes in equity markets.

We think it’s important to stay abreast of what the market itself is telling us through relative strength. When combined with your own fundamental ETF ideas, this market-generated information can be the key edge you have in terms of finding profitable entries and exits.

As we proceed further into the 2nd half of 2010, we have every intention of finding market segments that stay consistent with our global relative strength models. Near-term, look for pullbacks in some of the improving relative strength ETFs to make any adjustments necessary to your portfolios net exposures.