Apr 20, 2010

in Relative Strength, Video

4 minute video going over a few recent examples:

Feb 24, 2010

in Correlation

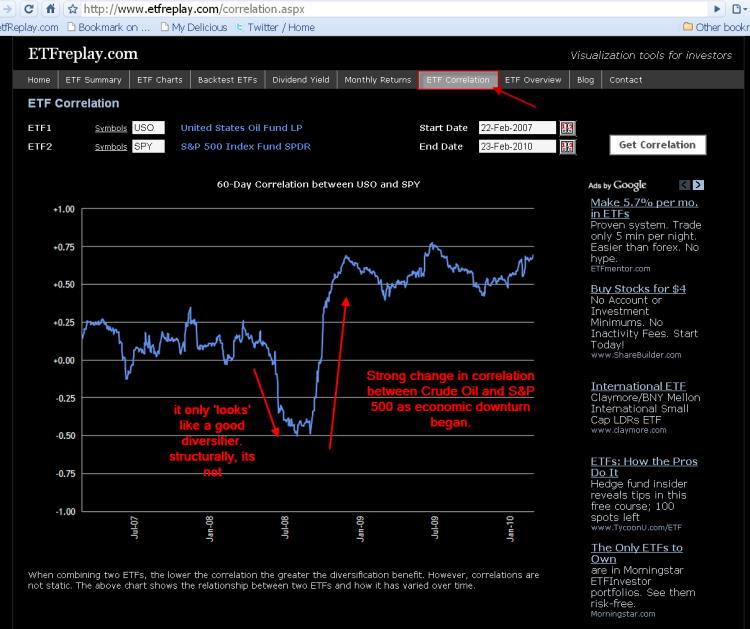

I know that this may be implied by others --- but its not enough that something simply be non-correlated to be included in a portfolio. It also needs to have positive expected return.

Structurally speaking, commodities markets are both 1) quite volatile and 2) generally quite sensitive to the overall economy -- which is what the stock market is sensitive to. In times of crisis, its been shown over and over again that correlations generally rise, so that you thought you were getting non-correlation, but instead you just get a more volatile asset that delivers an even larger drawdown for your portfolio. An excellent example is what just happened with crude oil in 2008, see images:

Jan 26, 2010

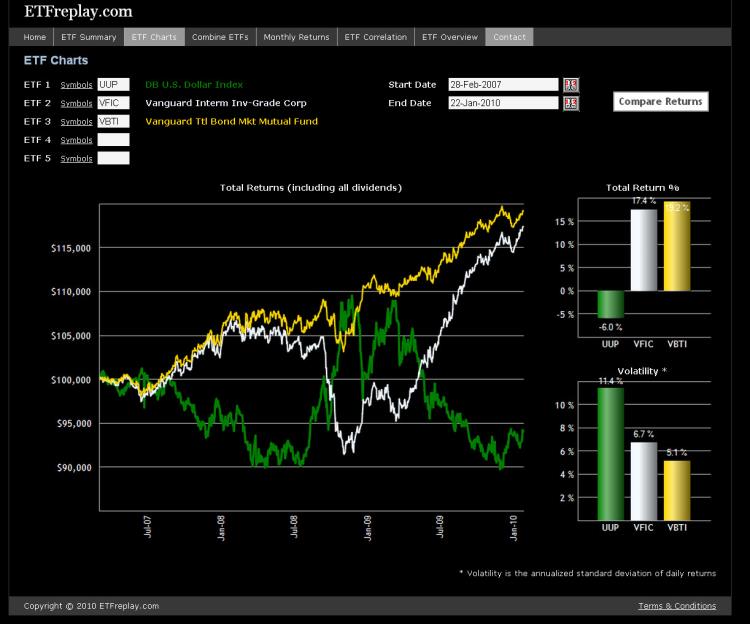

What has currency done to US bond market returns for foreign investors? While various currencies have performed notably differently, the overall Deutsche Bank Dollar Index ETF is a good proxy to make a weighted judgment of overall effect. Since February 2007, when the UUP was launched, there has been a depreciation of the dollar of about -6%. With domestic currency bond market index returns in the +17 to +19% over this period and understanding that some currencies fared much better or worse than the underlying DB dollar index, you can see that currency can be quite a meaningful contribution to overall return.

To update this chart to today or visualize similar relationships using other ETF combinations, go here: http://www.etfreplay.com/charts.aspx

Jan 23, 2010

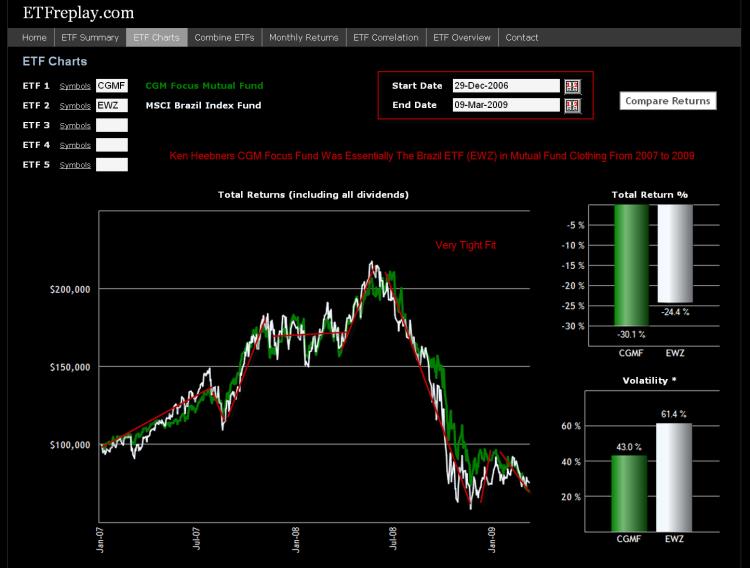

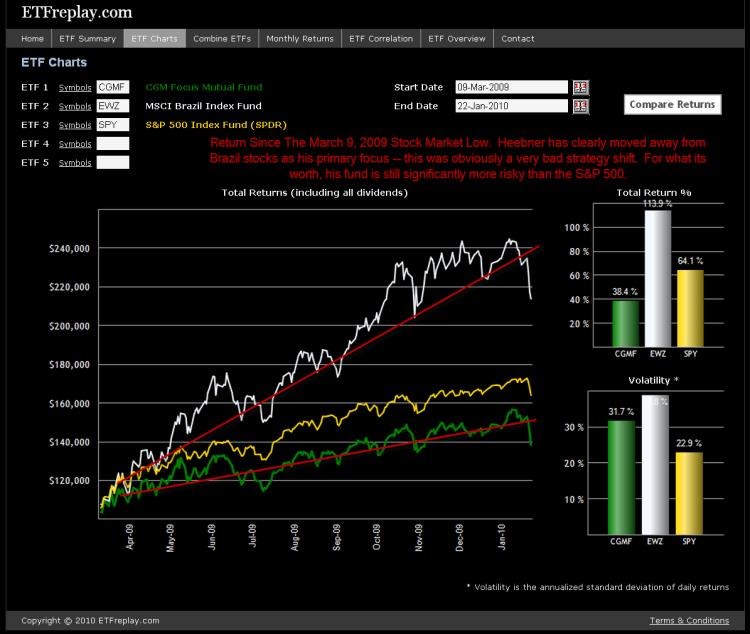

Ken Heebner is considered one of the very best fund managers in the country. But during this period of time, his fund was simply no different than the Brazil Fund ETF. This is an example of a fund manager exposing customers to a risk factor that they could have purchased in an ETF at a significantly lower fee. While Heebner should be credited for his outstanding long-term track record, his value-add -- like nearly all fund managers -- is in choosing broad risk expsosures, not 'stock-picking'. Moreover, he exposed customers to tremendous risk -- which could have been easily recognized if tracking his daily standard deviation of his funds returns -- as ETFreplay.com does.

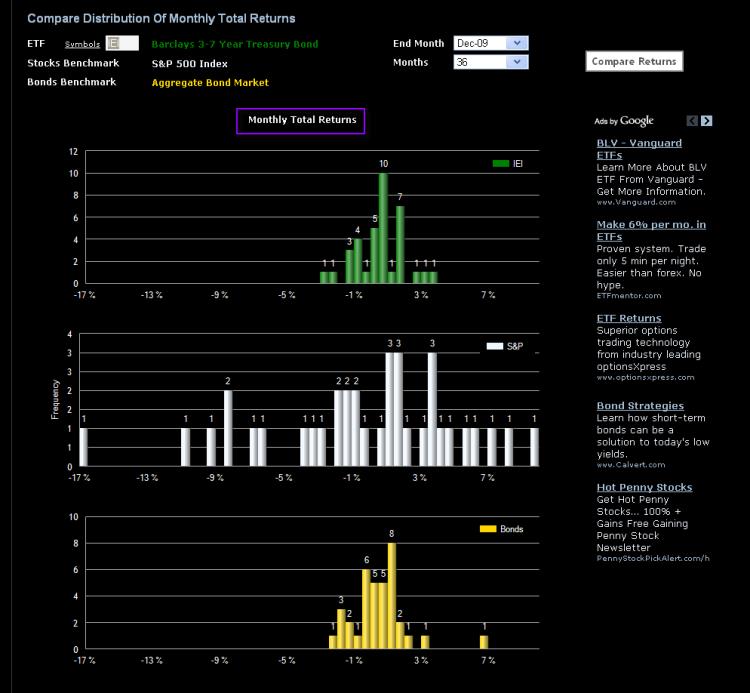

Jan 20, 2010

This particular ETF, Barclays 3-7 Year Treasury Bond ETF (symbol IEI) with a stated effective duration of approximately 4.5 years, had daily standard deviation of 5.5% in 2009. While yields on treasuries are low -- duration management below 5 years is inherently low relative risk.